Plans face numerous risks that fall into broad categories, including financial (interest rate, inflation, credit, market, liquidity, longevity) and funding (contribution, sponsor solvency, regulatory). Strategies such as liability-driven investing (LDI) and pension risk transfer (PRT) can be employed to manage these risks.

This white paper sheds light on the many challenges those governing plans face when considering different pension risk management strategies. It highlights how PFaroe DB with the right expert usage & input serves as a beacon, guiding them through these challenges by providing the necessary insights and a tool that makes it hard to miss any relevant financial consideration.

Key questions addressed include:

- What strategy is right for their plan?

- What impacts could each strategy create, both now and in the future?

- When should these strategies be implemented?

Knowing when to implement a PRT strategy is crucial, as it involves monitoring various factors like the plan’s funded status or changes in interest rates. PFaroe DB can monitor these factors daily and set up alerts for key stakeholders when specific thresholds are reached, enabling plan sponsors to act promptly.

This white paper assumes that the timing is favorable for implementing a strategy and aims to answer critical questions while providing a roadmap for effective pension plan financial risk management.

Buy-in vs. Buy-out

The table below highlights the differences between the two strategies used in pension risk transfers. While both strategies aim for effective pension risk management, they differ significantly in terms of implementation.

| Feature | Buy-Ins1 | Buy-Outs |

|---|---|---|

| Definition | An insurance policy where the pension plan buys a policy to cover the liabilities for a defined group of members but retains all legal and administrative obligations to those members. | An arrangement where the pension plan transfers the liabilities and legal (depending on jurisdiction) and administrative obligations for certain members to an insurance company. |

| Liability Ownership | Pension Plan | Insurance Company (if statutory discharge) |

| Boomerang risk | Minimized through Assuris Coverage 2 (10% of aggregate pensions remain at risk) | If no statutory discharge: Reduced up to 100% through Assuris coverage2 although some residual exposure may exist after other avenues are exhausted If statutory discharge: Eliminated |

| Member Status | Members remain in the plan, and the plan continues to pay their benefits, being (typically fully) reimbursed by the insurer. | If statutory discharge, members are no longer members of the plan and become policyholders of the insurance company, who pays their benefits directly. |

| Impact on Plan Assets | Policy becomes an asset of the pension plan. | Plan assets are used to purchase buy-out and in the case of a statutory discharge are not part of the plan anymore. |

| Risk Mitigation | Primarily addresses longevity risk and investment risk for the covered liabilities. | Transfers all risks to insurer3. |

| Flexibility | Buy-ins can be a step towards a full buy-out but offer flexibility to remain as a long-term strategy. | Once completed and in the case of a statutory discharge, the buy-out represents a full settlement of the obligations for the transferred members. |

| Cost (including advisers) 4 | In some cases, can be overall less expensive than buy-outs (with full or partial wind-ups) due to the retention of liabilities and the absence of a full legal transfer of obligations. | In some cases, can be overall more expensive due to the complete transfer of liabilities and the associated administrative and legal complexities. |

| Regulatory and Accounting Impact | The plan remains responsible for regulatory compliance and financial accounting reporting for the covered members. | Regulatory (depending on jurisdiction and statutory discharge) and financial accounting reporting are no longer required by the plan for the transferred members. |

2 In the case of the insurer’s insolvency: Under a buy-in, the contract is protected with Assuris coverage at a minimum of 90% of the aggregate benefits under the contract. Under a buy-out, Assuris protection is by member and covers benefits to the maximum of $5,000 per month or 90% of the benefit. Members with large benefits receive 100% Assuris coverage through the issuance of more than one policy in the case of a buy-out. Assuris would work closely with regulators, liquidators and solvent insurers.

3 Regulatory legal risk is only transferred if members’ jurisdiction allows.

4 Insurer premiums generally will not materially differ, if at all, between a buy-in and buy-out in Canada.

Using an external tool can help clearly define the impacts of various strategies. PFaroe DB can assist clients by isolating specific groups of members for transactions and providing key monitoring to ensure actions are taken at the right time. The choice between buy-ins, longevity hedges and buy-outs significantly affects the plan’s risk profile, regulatory compliance, and financial strategy, making it crucial for plan sponsors to carefully consider the implications of each approach.

Consideration

Having established the foundational differences between buy-in and buy-out strategies, it is essential to explore their potential repercussions, particularly in relation to longevity risk, asset allocation and hedging strategies, and their influence on the funded status of pension plans both in the immediate term and going forward. This examination will delve into how each strategy navigates the challenge of ensuring pension plan solvency amidst the unpredictability of beneficiary lifespans, adjusts the investment and risk mitigation approach, and ultimately affects the plan’s ability to meet its long-term obligations. Comparisons will also be made to other strategies that remove significant, but not necessarily as much risk such as LDI. Understanding the dynamics and differences is crucial for pension plan sponsors & fiduciaries as they make strategic decisions that will shape the financial health of their plans for years to come.

To help think through these points, let’s introduce a case study that covers three potential approaches to managing pension risk for a pension plan required to follow the Ontario Pension Benefits Act funding rules, totalling $1bn of liability (on a going concern basis), with pensioner liability representing approximately 50% of total plan liability:

- Implement an LDI strategy to fully hedge the pensioner portion of the plan (labelled “Pre PRT” in charts below)

- Implement a buy-in to fully hedge both market and longevity risks associated with the pensioner portion of the plan

- Implement a buy-out to remove all risks associated with the pensioner portion of the plan

For simplicity of analysis, all three approaches follow the same asset allocation for the non-pensioner portion of the plan (a 55/45 blend between liability hedging and return seeking assets).

The plan is assumed to be 115% funded on a going concern basis (and approximately 95% on an accounting and solvency basis) before any approach is implemented and the cost of buy-in/buy-out is assumed to equal the solvency (and IAS19) pensioner liability. Current service cost for the remaining active participants is $20m per year on a going concern basis.

Impact

Understanding the impact of different pension risk management strategies on the plan’s key metrics is a multifaceted challenge that requires complex analysis to be performed. Beyond the plan’s unique characteristics and the different PRT strategies under consideration, each key liability measure also has specific nuances that need careful thought before any implementation decision can be formulated.

On a going concern basis, the liability discount rate is based off the expected return on plan assets. In this case, undertaking a pensioner buy-out has a positive impact on the resulting discount rate as the allocation post buy-out has a higher proportion of return seeking assets (relative to the LDI strategy) leading to a higher expected return and a higher discount rate for the remaining plan. This positive impact is partially offset by a higher Provision for Adverse Deviation (PfAD) load being applied to the going concern liability. Meanwhile, under the buy-in strategy, because the assets and liabilities associated with the buy-in remain part of the plan, the going concern liability will reflect a blend of discount rates based on the higher proportion of return seeking assets and a rate that reflects the value of the buy-in annuity.

Under the solvency basis, the buy-out strategy is slightly negatively impacted in this case study. The annuity purchase discount rate is determined using the duration of the portion of the plan that is assumed to be settled by the purchase of annuity. Under prevailing conditions and guidance, the implementation of a pensioner buy-out dramatically increases this duration post-transaction which leads to a small drop in the annuity purchase discount rate due to the discount rate reducing at very high durations.

The buy-in approach introduces an interesting concept to the valuation of the plan’s assets. The pensioner buy-in value is dependent on the liability measure, i.e. the buy-in asset value may differ depending on whether the liabilities are valued on an accounting, solvency or going concern basis. Being able to accurately value the buy-in asset under different liability measures is a key aspect to the successful implementation of this strategy.

Taking all of these facets together means the impact on a residual plan’s key risk metrics following the implementation of PRT is not clear without performing detailed analysis. Multiple perspectives, discussed in the subsequent sections, should be considered depending on the goals and tolerances of the relevant stakeholders.

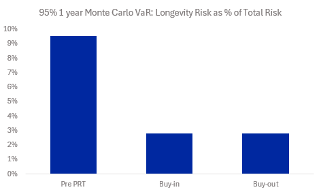

Longevity Risk

In the realm of pension plan management, a critical component of financial decision-making involves securing sufficient assets to meet the obligations to pensioners, particularly in scenarios where the lifespan of participants extends beyond the initial actuarial assumptions. Managing this longevity risk is fundamental when devising a comprehensive pension risk management strategy, aimed at safeguarding the financial health and sustainability of pension plans.

The mitigation of longevity risk is where PRT strategies fundamentally differ from LDI strategies as the latter is purely focused on the mitigation of economic risks. Under a buy-in arrangement, the plan acquires an insurance policy to ensure the pensions of all covered pensioners, thus transferring the longevity risk to the insurance provider and retaining the obligations on the plan’s balance sheet. In contrast, the buy-out method along with a statutory discharge involves the total transfer of pension liabilities to the insurer, eliminating these obligations from the plan’s balance sheet and thereby ending the plan’s exposure to longevity risk.

As illustrated by the chart below, opting for a PRT strategy has a significant beneficial impact on the plan’s exposure to longevity risk. However, it is crucial to note that the choice of PRT strategy—whether a buy-in or buy-out—yields a comparable effect on this risk aspect.

Different approaches can be taken to quantifying longevity risk – most relying on mathematical statistical uncertainty only. However, working together with Moodys, TELUS Health would also be able to consider RMS LifeRisks modelling, which quantifies longevity risk by simulating future mortality improvements using medical, demographic, and socioeconomic drivers as well. It supports scenario analysis, planning, and risk mitigation by projecting long-term outcomes under various assumptions.

Contribution Strategy

Understanding future contribution requirements is crucial for a pension plan aiming to minimize or eliminate the necessity for additional contributions while managing future obligations. By examining multi-year stochastic projections, you can clearly assess the influence on expected plan contributions over the next decade.

The chart uses percentiles to enable a quick visual of the potential annual contributions range both before and after implementing a PRT strategy. By leveraging this data, pension plans can quickly assess various scenarios, from the most favorable to the least, to determine the option that best fits their risk tolerance and to gauge the impact of future contribution requirements.

In this case, the three strategies drive quite different outcomes over the 10-year time horizon due to the regulatory framework that drives the determination of contribution requirements.

Alongside the reduction in longevity risk that comes from implementing the buy-in strategy, there is also a less obvious benefit that arises from this strategy. This is the favorable treatment of the buy-in for the purposes of determining the PfAD. Under the buy-in scenario, the PfAD load to the going concern liability is reduced from the Pre PRT scenario as the portion of the liabilities backed by the buy-in is exempt from the PfAD. This has the benefit of reducing the going concern liability that requires funding.

Under the buy-out strategy, an immediate top-up contribution of just under $30m is assumed to be made to ensure the solvency funding level remains equal to the Pre PRT funding level. With the pensioner liability now removed, the remaining plan has a significantly higher duration which leads to the liability being more sensitive to changes in interest rates. This in turn drives an increase in funding level volatility and given the interplay between funding level and the determination of contribution requirements, a wider range of contribution outcomes arises. Contrasting with the buy-in strategy, the median contribution levels are comparable, but there is a higher likelihood of a higher contribution under the buy-out strategy (assuming no further changes to investments).

Monitoring

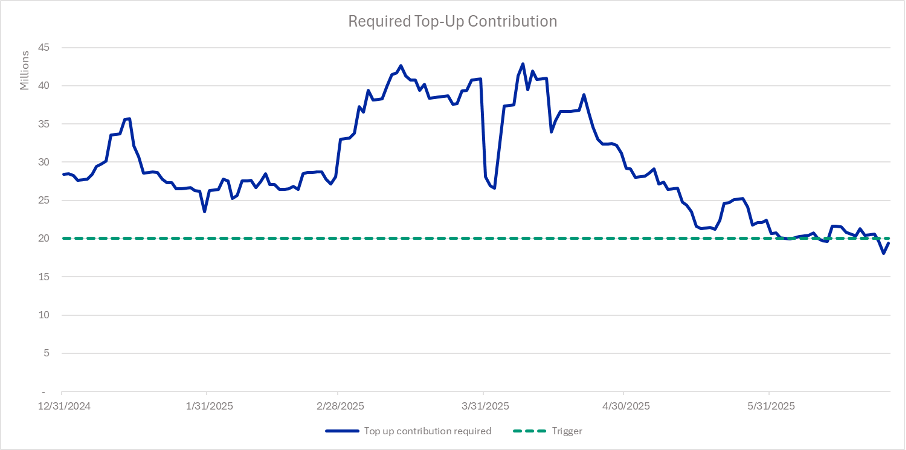

In addition to performing a comprehensive review of potential PRT strategies, there is also the important consideration of timing the execution of the selected strategy to optimize outcomes. Accurate and timely daily monitoring of key metrics ensures opportunities to transact are not missed. As an example, in this case study, the plan sponsor decides they wish to enter into the buyout strategy, but they would like the immediate contribution requirement to ensure the post buyout solvency level remains at the same level as before the buyout to be no more than $20m. Considering only financial market movements, the chart below shows how over the course of 2025 such opportunities have arisen in late Q2.

This is just one example where daily monitoring can be valuable. Monitoring daily solvency liabilities or market yields to drive effective decisions around timing of implementation are other commonly used approaches.

Engaging PRT Consultants and Planning Annuity Purchases

TELUS Health distinguishes itself in the field in Canada through expert management of complex plan modeling and agility in responding to uncertain market conditions. Their edge is reinforced by a combination of internal expertise and the strategic use of innovative external risk management technologies, such as PFaroe DB. This blend significantly bolsters the quality of advice. Their ongoing conversations about PRTs and other strategic options with clients underscore dedication to providing comprehensive insights and analyses. TELUS Health is committed to equipping clients with the necessary information to make informed decisions regarding their pension plans, ensuring these decisions are in harmony with their strategic objectives and lead to optimal results.

As the leading Canadian-headquartered PRT adviser by market volume in 2024 according to industry statistics, they also have the experience and relationships with insurers and reinsurers to support clients in influencing PRT pricing beyond responses to market movements. This will include deal structuring, proper data preparation and credibility that can reduce cautionary margins in insurer pricing.

As highlighted in this paper, Pension Risk Transfers do not adhere to a one-size-fits-all approach, even before operational, legal, data and deal dynamics come into play (and those firmly reinforce that conclusion). Even on just the raw financial risk aspects, a bespoke strategy is critical, considering the unique effects on your pension plan, encompassing overall risk (Value at Risk, VaR), longevity risk, asset allocation, contribution strategies, and the present funded status. This approach allows for a decision-making process that is best aligned with your plan’s requirements. TELUS Health’s systems support the daily monitoring of your plan, enabling timely and strategic PRT implementations. The analytical process also anticipates strategies for the effective management of remaining assets and liabilities after a PRT.

For the purposes of simplicity within this paper’s analysis, the asset allocation remained unchanged post-PRT. Still, in application, TELUS Health would typically help clients strategize anew, considering the shifts in liability duration and plan objectives after a PRT. In this arena, PFaroe DB again can support with powerful analysis and insights to allow optimal data-driven decision-making. Adjustments can ensure the establishment of a fitting hedging strategy, the management of appropriate asset risk levels, and the alignment of your plan’s future projections with its strategic goals. Their recommended best practice approach involves a collaborative process with clients at every stage, engaging with insurers and ensuring asset alignment both before and after the transfer, optimizing a plan’s performance to meet its objectives.

Conclusion

In conclusion, the landscape of pension plan management is becoming increasingly complex, necessitating a strategic, informed approach to decision-making. This white paper has demonstrated the critical role advanced tools like PFaroe DB play in navigating this complexity, offering real-time data and analytics that empower pension plan managers to make decisions that are both timely and informed. Through a detailed exploration of buy-ins and buy-outs, we have underscored the importance of understanding the nuanced impacts these strategies have on a plan’s risk profile, regulatory compliance, and financial health. By leveraging PFaroe DB with the right consultant for daily monitoring and strategic decision-making, pension plans can not only respond proactively to market dynamics but also align their management practices with long-term objectives, ensuring a secure financial future for their beneficiaries. This paper reaffirms the need for a bespoke approach to Pension Risk Transfers, one that considers the unique characteristics of each pension plan, to navigate the challenges of today’s pension landscape effectively.