CDI – From Idea to Reality

Introduction

Cashflow Driven Investment has always been an aspiration within the DB Pensions World in some shape or form. Over recent years an increasing number of asset managers and consultants in the DB space have been advising clients on the merits of incorporating CDI strategies in their broader portfolio allocation strategy. Now, data drawn from PFaroe’s growing client base of both asset owners and managers – covering over £1.0tn of assets – suggests this is finally becoming a reality. In the words of Victor Hugo “nothing is stronger than an idea whose time has come”

Why CDI

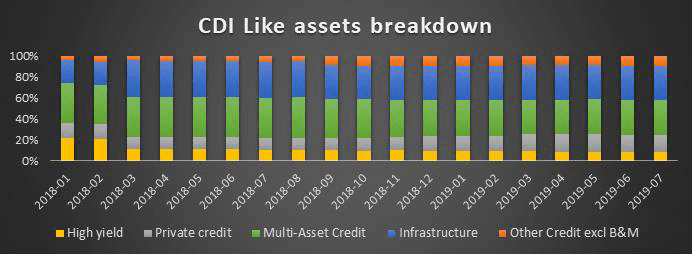

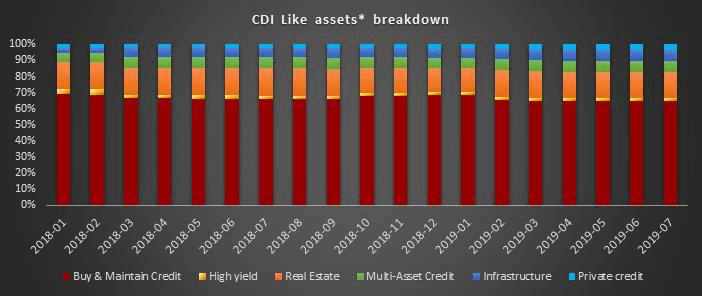

CDI is a strategy which relies on matching the timing of the underlying cash (in)flows on the asset side with the cash (out)flows on the liability side. In addition, CDI is also a strategy which, by design, is trying to provide better return, on a risk adjusted basis, compared to some of the traditional portfolio asset combinations of equities and bonds. This is usually achieved by re-allocating some of the return-seeking part of the portfolio into more alternative types of assets – for example, private credit, infrastructure investments, insurance-linked securities, ground rent, and other similar instruments – which rely on steady (often secured) cashflow streams with a lower (on average) probability of default over the duration of the respective asset. These private credit-like investments have inherent illiquidity premium compared to similarly rated, publicly traded credit instruments.

CDI’s journey through a PFaroe lens

The popularity of CDI, as a concept at least, has been growing over the last couple of years, as many asset managers and consultants have been promoting CDI as a key component of the DB Pension Scheme asset mix. However, it has been hard to quantify the progress that has been made. Some would argue that CDI is still in its early stages and various hurdles – such as greater assurance on the realization of the promised cashflows for the duration of the investment period and, of course, improved funding levels – need to be addressed before CDI firmly takes its place at the centre of the DB pension plan portfolio. While many would agree that the above is true, we analysed PFaroe’s 3000 pension plans, with over £1tn of investments, to test the hypothesis that CDI is being placed more and more at the center of the broader portfolio mix.

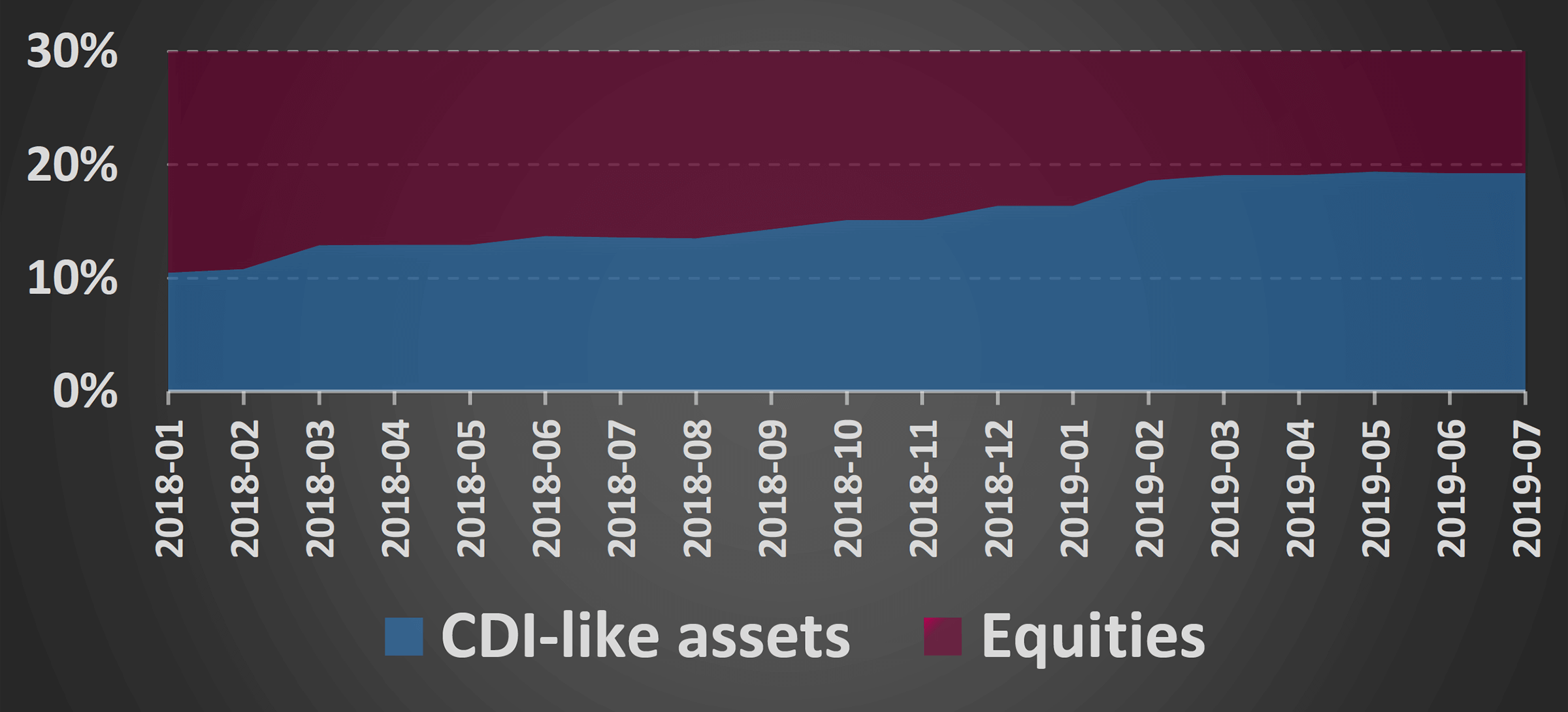

The chart above shows the allocation to equities vs CDI eligible assets (such as infrastructure, private and multi-asset credit, but excluding the alternative strategies which follow their natural course within the average pension plan portfolio, such as hedge funds and private equity). It is clear to see that the overall allocation to CDI eligible assets has more than doubled over the last 18 months (since 0% 10% 20% 30% 2018-01 2018-02 2018-03 2018-04 2018-05 2018-06 2018-07 2018-08 2018-09 2018-10 2018-11 2018-12 2019-01 2019-02 2019-03 2019-04 2019-05 2019-06 2019-07 CDI-like assets Equities the beginning of 2018) and at the same time, return-seeking equity-like investments are decreasing at a similar rate. This is more subtle than the previous decade’s move from equities into bonds and further analysis of the data shows that one of the biggest drivers has been increasing allocations to infrastructure investments, specifically.

The investment trend to disinvest from equities during periods of recession and invest instead into fixed income types of instruments has been well tested over time. Many consultants and managers may well be anticipating a recession in the next 12-24 months which would make the case for steady cashflow and fixed income assets even stronger for a well-funded DB pension plan. While no one knows for a fact when the next recession will kick in, one thing is certain – with or without a recession, the last 18 months of data is showing us a clear picture: CDI is not just an idea but a strategy whose time has come. At a time where CDI is playing an increasingly important role within the broader portfolio strategy, ready access to asset and liability data and being aware of both broader asset and liability trends is becoming increasingly important to both the asset owner and the growing asset manager client base. Moreover, in further support of the data above, we are seeing an increasing number of clients who are using the functionality of PFaroe to help them test and build more robust CDI strategies within their asset portfolios, along with monitoring their allocations across multiple portfolios and clients.

Disclaimer

This document contains proprietary information that is confidential, constitutes intellectual property of Risk First Group Limited or an affiliate (Risk First) and may be subject to legal privilege. If you have a confidentiality or non-disclosure agreement with Risk First, this document constitutes confidential information of Risk First. You may not copy or distribute this document or any information contained in it to any other person except as required by law, regulation or appropriate court order or by written agreement from Risk First. Although reasonable care has been taken by Risk First to ensure that the facts stated, opinions given and projections made in this document are fair and accurate, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy or completeness of the information, opinions, estimates or projections contained in this document. Neither Risk First nor any other person accepts any liability for any loss arising from any use of this document or its contents or otherwise. The information and/or recommendations contained in this document are given as at its date of publication and are subject to change without notice. This document is not an offer for sale, invitation to treat or subscription of or solicitation of any offer to buy or subscribe for any securities nor shall it form the basis of or be relied on in connection with or act as an inducement to enter into any contract or commitment. Risk First is not acting on your behalf and will not be held responsible for providing you protection in this matter.